Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle sits down with former Senate Majority Leader Emeritus Robert Hertzberg to discuss the proposed Middle-Class Homeownership and Family Home Construction Act.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

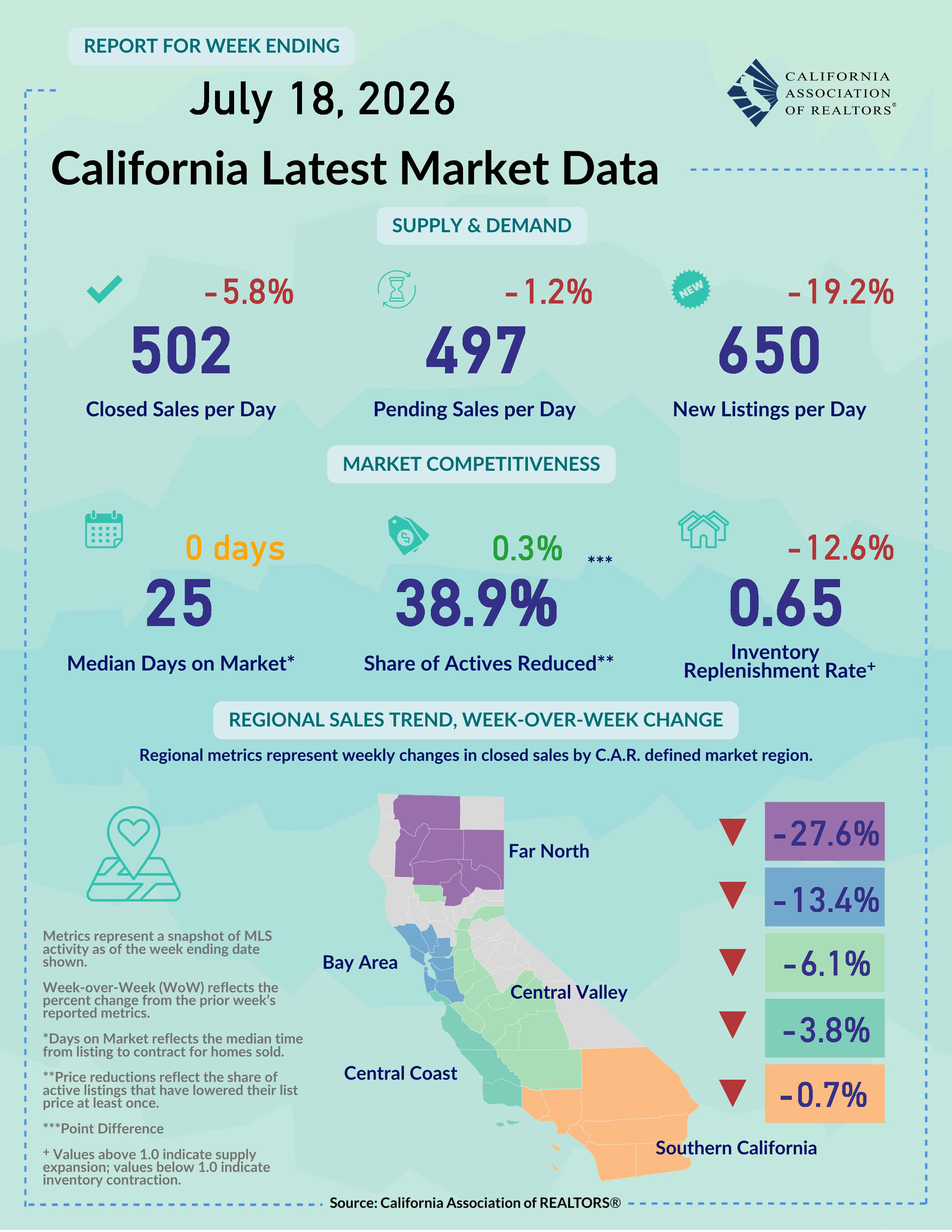

July 20, 2026 - Economic data released this week painted a picture of an economy that continues to slow gradually rather than contract. Inflation cooled more than expected, retail spending remained resilient, and the Federal Reserve gained some reassurance that underlying price pressures may be easing. However, renewed conflict in the Middle East has reignited inflation concerns by pushing oil prices higher, raising the risk that recent progress on inflation could prove temporary. As a result, mortgage rates have moved higher again as the market reassessed the inflation outlook. Meanwhile, homebuilders remain cautious amid elevated financing costs and affordability challenges. For California's housing market, limited inventory should continue to support home prices, but renewed upward pressure on mortgage rates could temper buyer demand and slow the momentum that emerged in the second quarter of the year. Inflation Cools More Than Expected, but Fed Remains Cautious: Inflation showed encouraging signs of moderation in June, as both consumer and producer prices came in softer than expected. The headline Consumer Price Index (CPI) posted its largest monthly decline since April 2020, driven by falling energy prices and slower growth in shelter and other service costs. Core inflation eased to 2.6% year over year and had the smallest month-over-month gain since December 2020. Producer prices also declined, although elevated business input costs suggest underlying inflationary pressures have not fully dissipated. While the reports might have lowered the immediate urgency for additional monetary tightening, Federal Reserve officials reiterated that several months of favorable inflation data will be needed before considering lowering interest rates. Consumer Spending Holds Up Well Despite Slower Growth Pace: U.S. retail sales rose again but at a slower pace in June as consumers spent less at gas station due to falling energy prices. June’s retail sales report released by the Commerce Department shows that non-inflation adjusted sales for retail trade and food services went up by 6.7% from June 2025, a decline from the revised 7.3% reported in the prior month. Excluding spending at the pump, retail sales were still up 5.7% from a year ago, which was just a slight dip from the 5.8% registered in May. Sales generally increased across major sectors, with auto sales showing a solid increase of 5.7%, while non-store retailers jumped 14.2% from a year ago, likely due to Amazon Prime Day moving to late June this year. On the other hand, annual sales growth pace for grocery stores (0.9%) and health & personal care stores (0.2%) were soft last month, suggesting that there are weaknesses in spending on consumer essentials. If the trend continues in the next couple months, it will further slowdown consumer expenditure and put a drag on economic growth. Homebuilding Remains Weak Despite Starts Beating Estimates: The U.S. homebuilding sector continues to face mounting challenges despite a rebound in overall housing starts in June, driven almost entirely by multifamily construction. Single-family activity remained weak, with housing starts declining for the third consecutive month and building permits falling to their lowest level in ten months, as builders scaled back future projects in response to elevated mortgage rates, rising construction costs, and softer buyer demand. Meanwhile, after plummeting to the lowest level in recent years, multifamily starts surged 76.2% from May and jumped 17.2% from 12 months ago. While the sharp increase was welcome news for the sector, permitting activity remained soft as June’s modest monthly and annual declines in multifamily permits suggest weak construction activity in the sector in the near term. Home Sales Bounced Back but Higher Rates Could Test the Recovery: California's housing market gained momentum in June, with existing single-family home sales rising 4.1% from May and 6.0% from a year earlier — the strongest annual increase in nine months. Sales growth broadened last month, with six of the seven major price segments posting double-digit gains and all five major regions recording year-over-year increases. For the first half of 2026, statewide sales were up 1.9% from the same period last year, providing hopes that the market is still on course to see a gain for the year as a whole from last year despite elevated mortgage rates. The recent resurgence of conflict in the Middle East, however, has renewed concerns over higher energy prices and inflation, pushing mortgage rates higher again and creating new headwinds for housing demand as the summer buying season continues. Tight Inventory Provides Support to Home Prices: California's median home price eased 2.8% in June after reaching a record high in May but remained above $900,000 for the third consecutive month. The modest 0.4% annual increase reflected both a more balanced mix of homes sold and slower price appreciation, as the share of million-dollar home sales declined from May's record level. Meanwhile, housing supply tightened further with active listings declining 10.4% from a year earlier, the fifth consecutive annual decrease. With the lock-in effect not completely going away in the near term and many homeowners remaining reluctant to put their properties up on the market, housing supply could stay tight throughout the remainder of the summer. As such, while prices are expected to soften seasonally during the second half of the year, housing supply shortage should help cushion non-seasonal price deterioration, limiting the likelihood of more pronounced declines if mortgage rates remain elevated. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|