Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Watch our C.A.R. economists provide updates on the latest housing market data and happenings... quickly!

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

REALTOR® Action FundLearn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

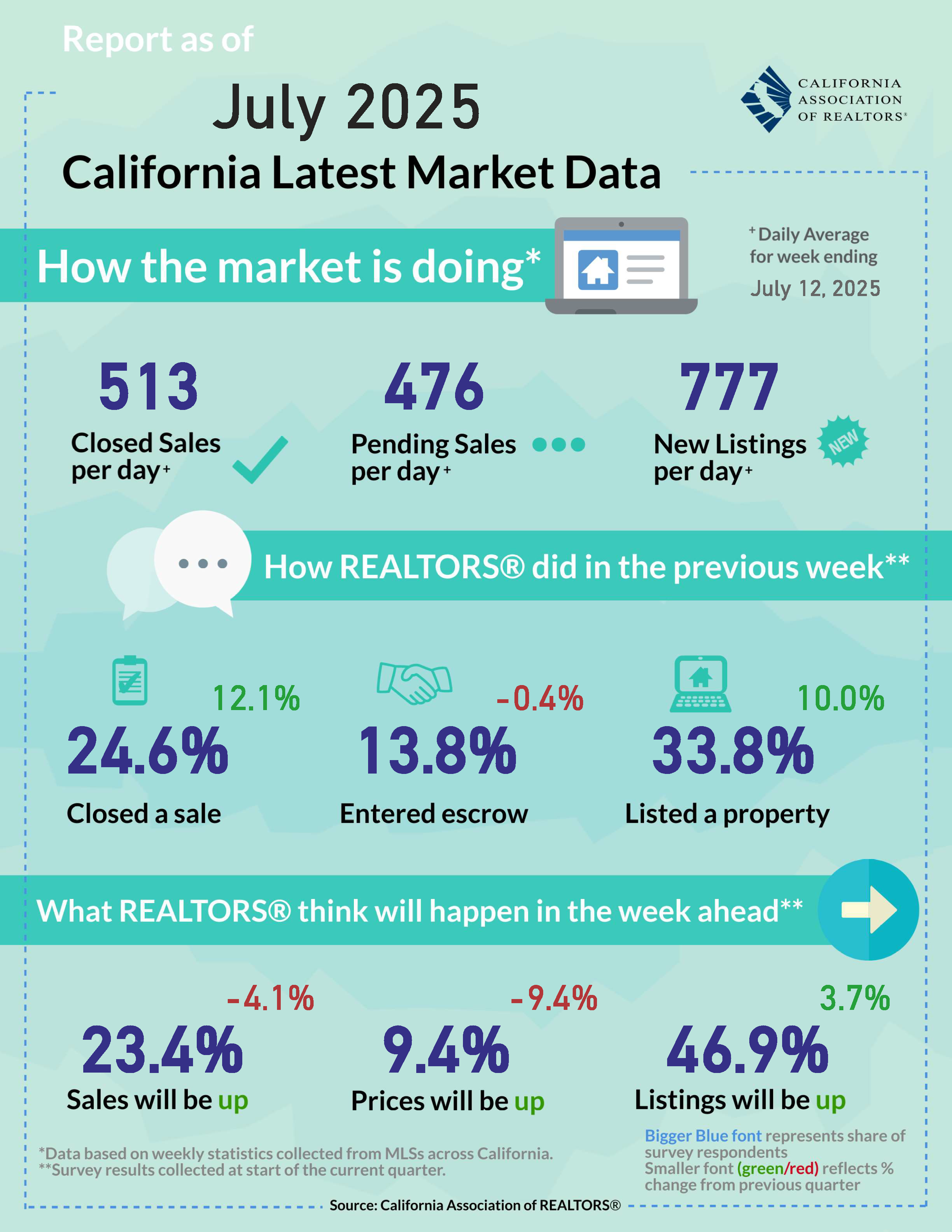

July 14, 2025 – In June, small business sentiment remained steady but was slightly dampened by rising inventories and concerns about taxes, although inflation worries eased and overall uncertainty declined. Meanwhile, mortgage application activity increased in early July amid easing interest rates, suggesting renewed buyer interest. However, homeowners face growing financial strain, with insurance premiums projected to rise 8% nationally and 21% in California due to natural disasters and construction costs. The 2025 C.A.R. Consumer Survey reveals many renters remain unprepared for homeownership, lacking financial knowledge and burdened by debt. At the same time, most California homeowners are choosing to stay put due to high mortgage rates and property taxes, tightening supply and making it harder for first-time buyers to break into the market. Small business optimism holds firm: In June, the NFIB Small Business Optimism Index remained steady, only decreasing 0.2 of a point to 98.6, slightly above the 51-year average of 98. A significant increase in small business owners reporting excess inventories was the primary factor behind the index’s decline. While the net percentage of owners expecting improved business conditions fell, it remained historically positive. For a second month in a row, taxes were identified as the top concern for 19% of small business owners, up one point from May. The percentage of owners citing labor quality as their primary issue held steady, remaining at its lowest level since April 2020. The proportion of owners reporting inflation as their main problem dropped to its lowest point since September 2021, but the net share of firms that raised average selling price soared four points last month, a reflection that inflation could climb in the months ahead. In terms of overall business health, 8% of owners rated their condition as excellent, 49% as good, 35% as fair, and 7% as poor. The drop of the uncertainty index by 5 points to 89 from May suggests that business owners feel slightly relieved by the improved visibility of trade policy but remain concerned about the current economic environment. Mortgage applications increase as rates ease: Mortgage applications rose by 9.4% on a week-over-week basis for the week ending July 4, 2025, as rates eased throughout the month of June. According to the Mortgage Bankers Association (MBA), the Refinance Index was up 9% from the prior week and was 56% higher than the same time last year. Meanwhile, the unadjusted Purchased Index dipped 13% from the prior week but increased 25% compared to the same week 12 months ago. In fact, after adjusted for seasonality, purchase applications reached the highest level of activity since February 2023. The average loan size dropped to $432,600, the lowest since January, while the average contract interest rate for 30-year fixed rate conforming loan mortgages dipped to a three-month low of 6.77%. The continuing increase in housing inventory, coupled with the slowdown in home prices, could help boost buyer demand heading into the second half of the year. Insurance premiums climb amid rising climate risks: According to the latest study by Insurify, homeowners across the nation can expect higher insurance premiums by the end of 2025, with costs projected to rise 8% annually to a national average of $3,520. The increase in premiums is driven by more frequent and severe natural disasters like wildfires, hurricanes, and hailstorms. For the nation, a typical homeowner will pay about $261 more over the next year. California, being a state where insurance premiums are rising the fastest, homeowners are facing an increase of 21%, bringing their average annual premium to $2,930. This hike is driven primarily by the continuing rising costs in construction but the recent wildfires in Los Angeles County also contributed to the increase in insurance premiums in the Golden State. Financial literacy on homebuying continues to be low among California renters: Renter financial literacy remains low, leaving many ill-prepared for homeownership, according to the California Association of REALTORS® 2025 Consumer Survey. Although 70% of renters are aware of their credit score, most lack essential knowledge about the home buying process. Specifically, 58% are unfamiliar with mortgage qualification criteria, 60% have not started saving for a down payment, and 84% are unaware of how much they would qualify for in regard to a home loan. Additionally, 83% of them are unaware of any first-time homebuyer program, with most renters citing a median down payment of 25% as the requirement to purchase a property. Debt is a large hurdle for renters entering the market, with 41% of them carrying credit card debts, 20% having a balance on their student loans, and 16% owing money to their auto loans, yet only 18% of renters know their debt-to-income ratio. California homeowners continue to stay put: According to the 2025 Consumer Survey conducted by the California Association of REALTORS®, many homeowners decided not to move in the last 12 months, likely due to continuing high costs of homebuying in the past few years. In fact, 73% of homeowners said they have not considered selling their home within the past year. California homeowners are staying put longer, with 22% planning to keep their homes for 0–4 years, down 3% from 2024 and down 5% from 2023. Meanwhile, there was an increase in homeowners planning to keep their homes for longer periods of time with 22% now planning to stay 15–24 years, up 3% from 2024 and up 6% from 2023. With today's elevated mortgage rates, many are financially incentivized to stay put. In fact, when asked about reasons not to sell, 60% of homeowners cited high mortgage rates and 57% of homeowners cited increased property taxes on a new property as important reasons not to sell their homes. The reluctance to move is a contributing factor to a housing market that remains tight, which makes it increasingly difficult for entry-level homebuyers to enter California’s already expensive housing market.

Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|